by Eric Price | Aug 19, 2024 | Front Page, MNPL, Perusals, Recent News, Recent News, Row 2

Are you SURE you are registered to vote? Want to make sure before it’s too late? Vote.org has got you covered! CLICK RIGHT NOW to see if you are registered. Check Registration Status Register to Vote It’s time to VOTE UNION! Both parties have made their...

by Eric Price | Jul 26, 2024 | American, Featured, Featured News, Front Page, Other News, Perusals, Recent News, Row 2, The Association, Uncategorized

July 26, 2024 All Association Members, Today, leaders from American Airlines, Inc. reached out to the Association leadership to discuss the possibility of exploring an economics only, short-term extension of existing JCBAs. American asked to schedule a meeting on...

by Eric Price | Jul 23, 2024 | Featured, Front Page, Other News, Perusals, Recent News, Recent News, Row 2

United Contract Negotiations Update 23 July 2024 Dear Sisters and Brothers, Last week, your IAM District 141 United Airlines Negotiating Committee met with company management to continue negotiations on the collective bargaining agreements (CBA) for several groups....

by Eric Price | Jul 22, 2024 | Featured, Front Page, Perusals, Recent News, Recent News, Row 2

Agreement Reached at Flagship Facility Services Dear Sisters and Brothers, IAM members at Flagship Facility Services located at the San Francisco Maintenance Base voted overwhelmingly to ratify a new three-year agreement. This Agreement creates new payscales that...

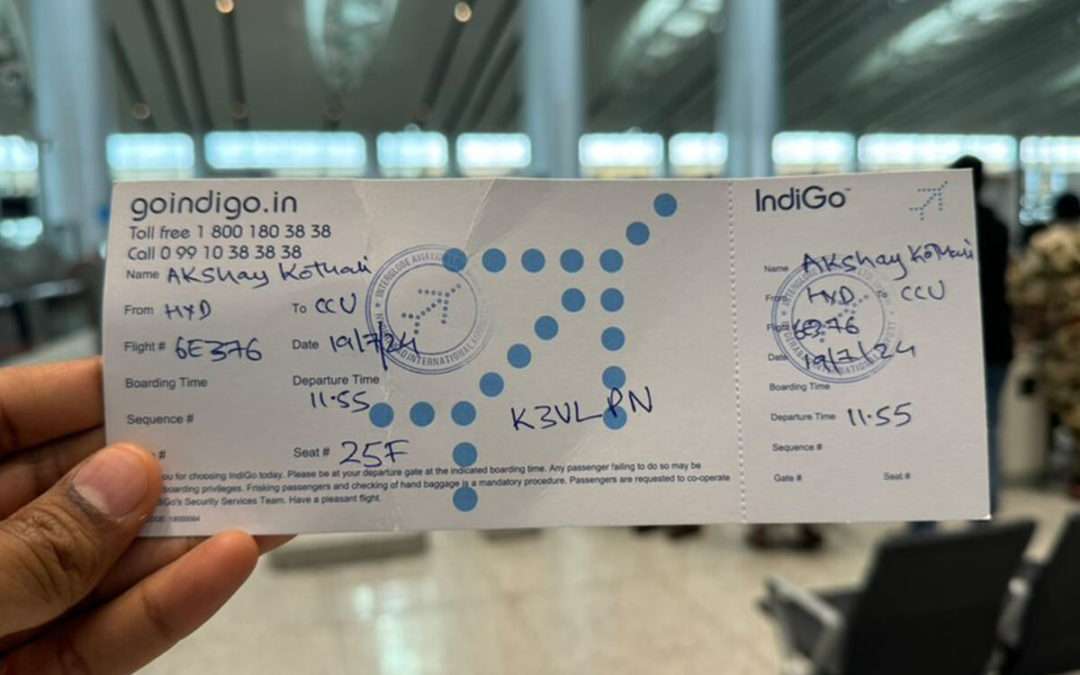

by Eric Price | Jul 19, 2024 | Featured, Featured News, Front Page, Other News, Perusals, Recent News, Recent News, Row 2

Microsoft Update Triggers The Largest Tech Disaster in History Pictured: a passenger posts an image of a handwritten boarding pass. Microsoft Update Triggers The Largest Tech Disaster in History IAM141.org 19 July 2024 On Friday morning, a global computer outage led...

by Eric Price | Jul 18, 2024 | Featured, Featured News, Front Page, MNPL, Other News, Perusals, Recent News, Recent News, Row 2

Supreme Court Strikes At Federal Experts Supreme Court Strikes At Federal Experts IAM141.org 18 July 2024 WASHINGTON – On June 28, 2024, the U.S. Supreme Court issued a landmark decision that will drastically alter the government’s ability to enforce...